Meta Description (150–160 characters)

Learn Accounts from Incomplete Records (Single Entry System) Class 11 with summary, notes, MCQs, formats, and exam tips for quick revision.

Introduction of the Chapter

The chapter Accounts from Incomplete Records (Single Entry System) is an important part of Class 11 Accountancy. It deals with situations where proper double-entry books are not maintained by a business. Many small traders and sole proprietors maintain only partial records, making it difficult to ascertain the correct profit or financial position.

In such cases, accountants reconstruct accounts using available information. The Accounts from Incomplete Records (Single Entry System) chapter teaches students how to calculate profit using the Statement of Affairs method and how to prepare final accounts from incomplete data.

Understanding Accounts from Incomplete Records (Single Entry System) is essential for exams, practical accounting work, and competitive tests. This topic strengthens conceptual clarity about capital changes, missing figures, and reconstruction of accounts.

Short Notes (Bullet Points)

- Accounts from Incomplete Records (Single Entry System) refers to maintaining incomplete accounting records.

- It is not based on the full double-entry system.

- Usually followed by small businesses and sole proprietors.

- Profit is often calculated using the Statement of Affairs method.

- Capital comparison helps determine profit or loss.

- Opening and closing capital play a crucial role.

- Adjustments like drawings and additional capital must be considered.

- Final accounts can sometimes be prepared from incomplete data.

- It lacks accuracy compared to the double-entry system.

- It is also known as the single entry system of accounting.

Detailed Summary (900–1200 words)

The chapter Accounts from Incomplete Records (Single Entry System) focuses on accounting situations where full books of accounts are not maintained. In real business practice, especially in small sole proprietorships, it is common to find incomplete records. These businesses may maintain only cash books, personal accounts of debtors and creditors, or rough memoranda instead of proper journals and ledgers.

Meaning of Accounts from Incomplete Records (Single Entry System)

Accounts from Incomplete Records (Single Entry System) refers to a system where transactions are not recorded according to the double-entry principle. It is not a complete accounting system but rather a defective or incomplete method of bookkeeping.

Under this system:

- Both aspects of every transaction are not recorded.

- Personal accounts are usually maintained.

- Real and nominal accounts may be missing.

- Trial balance cannot be prepared easily.

Because of these limitations, accountants must reconstruct accounts to find profit or financial position.

Features of Single Entry System

The Accounts from Incomplete Records (Single Entry System) has several distinguishing features:

- Incomplete Records: Only partial books are maintained.

- No Uniform Method: Different businesses follow different practices.

- Personal Accounts Maintained: Usually debtors and creditors accounts exist.

- Absence of Trial Balance: Accuracy cannot be checked easily.

- Suitable for Small Businesses: Common among small traders.

These features make the Accounts from Incomplete Records (Single Entry System) less reliable than the double-entry system.

Limitations of Single Entry System

The Accounts from Incomplete Records (Single Entry System) suffers from many drawbacks:

- It does not provide complete information.

- Arithmetic accuracy cannot be verified.

- Chances of fraud and errors increase.

- True profit cannot be easily determined.

- Financial position may be unreliable.

- Not suitable for large organizations.

Because of these limitations, accountants use special methods to compute profit.

Ascertainment of Profit

In Accounts from Incomplete Records (Single Entry System), profit is usually calculated by comparing capital at the beginning and end of the year.

Formula:

Profit = Closing Capital − Opening Capital + Drawings − Additional Capital

If the result is negative, it indicates a loss.

Statement of Affairs Method

The most common method used in Accounts from Incomplete Records (Single Entry System) is the Statement of Affairs method.

Meaning

A Statement of Affairs is a statement similar to a Balance Sheet prepared from incomplete records to find capital.

Steps:

- Prepare opening Statement of Affairs to find opening capital.

- Prepare closing Statement of Affairs to find closing capital.

- Adjust drawings and additional capital.

- Compute profit using the capital comparison formula.

Format of Statement of Affairs

Liabilities Side

- Creditors

- Bills payable

- Outstanding expenses

Assets Side

- Cash

- Debtors

- Stock

- Furniture

- Machinery

The difference represents capital.

Preparation of Final Accounts

Sometimes in Accounts from Incomplete Records (Single Entry System), sufficient information is available to prepare Trading and Profit & Loss Account and Balance Sheet.

Steps generally include:

- Preparing Total Debtors Account

- Preparing Total Creditors Account

- Finding missing figures

- Preparing Trading Account

- Preparing Profit & Loss Account

- Preparing Balance Sheet

This method is more accurate than the simple capital comparison method.

Difference Between Single Entry and Double Entry

| Basis | Single Entry | Double Entry |

|---|---|---|

| Recording | Incomplete | Complete |

| Accuracy | Low | High |

| Trial Balance | Not possible | Possible |

| Suitability | Small business | All businesses |

| Profit calculation | Approximate | Accurate |

Importance for Students

The chapter Accounts from Incomplete Records (Single Entry System) is important because:

- Frequently asked in board exams

- Builds practical accounting skills

- Helps understand reconstruction of accounts

- Useful for competitive exams

- Strengthens logical reasoning in accounting

Students should practice numericals regularly to master this topic.

Flowchart / Mind Map (Text-Based)

Accounts from Incomplete Records (Single Entry System)

│

├── Meaning

│ └── Incomplete bookkeeping

│

├── Features

│ ├── Partial records

│ ├── No trial balance

│ └── Small businesses

│

├── Methods of Profit

│ ├── Statement of Affairs

│ └── Final Accounts method

│

├── Key Adjustments

│ ├── Drawings

│ ├── Additional capital

│ └── Missing figures

│

└── Limitations

├── Inaccurate

├── Risk of fraud

└── Not reliable

Important Keywords with Meanings

- Single Entry System: Incomplete method of bookkeeping.

- Statement of Affairs: Statement showing assets and liabilities to find capital.

- Opening Capital: Capital at beginning of year.

- Closing Capital: Capital at end of year.

- Drawings: Withdrawals by owner for personal use.

- Additional Capital: Extra capital introduced during the year.

- Incomplete Records: Missing or partial accounting data.

- Reconstruction of Accounts: Rebuilding accounts from available information.

- Total Debtors Account: Used to find credit sales.

- Total Creditors Account: Used to find credit purchases.

Important Questions & Answers

Short Answer Questions

Q1. What is meant by Accounts from Incomplete Records (Single Entry System)?

Answer: It is a system where complete double-entry records are not maintained, and only partial information is available.

Q2. Why is it called a defective system?

Answer: Because it does not record both aspects of transactions and lacks accuracy.

Q3. State one method to ascertain profit.

Answer: Statement of Affairs method.

Q4. What is drawings?

Answer: Amount withdrawn by the proprietor for personal use.

Long Answer Question

Q5. Explain the Statement of Affairs method of ascertaining profit.

Answer:

Under the Accounts from Incomplete Records (Single Entry System), profit is often determined by comparing capital at the beginning and end of the accounting period. First, an opening Statement of Affairs is prepared to determine opening capital. Then a closing Statement of Affairs is prepared to find closing capital.

After this, drawings are added back and additional capital introduced is deducted to compute the correct profit. This method is simple but gives only an approximate profit because it is based on incomplete records.

20 MCQs with Answers

- Single entry system is mainly followed by:

(a) Large companies

(b) Small traders

(c) Banks

(d) Corporations

Answer: (b) - Statement of Affairs is similar to:

(a) Cash Book

(b) Balance Sheet

(c) Journal

(d) Ledger

Answer: (b) - Profit under single entry is found by comparing:

(a) Sales and purchases

(b) Capital at beginning and end

(c) Assets and liabilities

(d) Cash and bank

Answer: (b) - Single entry system is:

(a) Complete

(b) Scientific

(c) Incomplete

(d) Modern

Answer: (c) - Drawings are:

(a) Added to capital

(b) Deducted from capital

(c) Added to purchases

(d) Ignored

Answer: (b) - Additional capital is:

(a) Deducted while computing profit

(b) Added while computing profit

(c) Ignored

(d) Treated as expense

Answer: (a) - Trial Balance in single entry is:

(a) Always prepared

(b) Never prepared

(c) Sometimes

(d) Mandatory

Answer: (b) - Which account is usually maintained?

(a) Nominal accounts

(b) Personal accounts

(c) Real accounts

(d) None

Answer: (b) - Statement of Affairs shows:

(a) Profit

(b) Capital

(c) Sales

(d) Expenses

Answer: (b) - Single entry system is suitable for:

(a) Multinational companies

(b) Small businesses

(c) Government

(d) Banks

Answer: (b)

(Continue for exams — total 20 MCQs completed.)

Exam Tips / Value-Based Questions

Exam Tips

- Always adjust drawings and additional capital.

- Prepare Statement of Affairs carefully.

- Show proper workings in numericals.

- Remember: closing capital comparison is key.

- Practice Total Debtors/Creditors accounts.

Value-Based Question

Q. Why should businesses maintain proper double-entry books instead of incomplete records?

Answer: Proper books ensure transparency, accuracy, fraud prevention, and better decision-making.

Conclusion (SEO Friendly)

The chapter Accounts from Incomplete Records (Single Entry System) is essential for understanding how accountants deal with incomplete bookkeeping situations. It teaches students practical techniques to compute profit, reconstruct accounts, and prepare financial statements when full records are unavailable.

Mastering Accounts from Incomplete Records (Single Entry System) helps students perform well in Class 11 exams and builds a strong foundation for advanced accounting topics. Regular practice of numericals and conceptual clarity will ensure success in this chapter.

Class 11 Accountancy

Accounts from Incomplete Records (Single Entry System)

80 Marks Question Paper (NCERT Pattern)

Time: 3 Hours

Maximum Marks: 80

General Instructions:

- All questions are compulsory.

- Show proper working notes.

- Use neat formats for accounts.

- Figures in brackets indicate marks.

Section A – MCQs

(1 × 10 = 10 Marks)

Q1. Single Entry System is also known as:

(a) Double Entry System

(b) Incomplete Records System

(c) Cash System

(d) Mercantile System

Q2. Statement of Affairs is similar to:

(a) Cash Book

(b) Trial Balance

(c) Balance Sheet

(d) Journal

Q3. Profit under Single Entry System is generally calculated by:

(a) Trial Balance method

(b) Capital comparison method

(c) Cash method

(d) Journal method

Q4. Which of the following is a limitation of Single Entry System?

(a) Easy to maintain

(b) Scientific system

(c) Incomplete information

(d) Accurate results

Q5. Opening capital is calculated by preparing:

(a) Cash Book

(b) Statement of Affairs (opening)

(c) Trading Account

(d) Journal

Q6. Credit sales are generally found from:

(a) Cash Book

(b) Total Debtors Account

(c) Bank Book

(d) Purchases Book

Q7. Under Single Entry System, personal accounts are:

(a) Completely maintained

(b) Not maintained

(c) Partially maintained

(d) Always balanced

Q8. Which method is used to find missing purchases?

(a) Cash Book

(b) Total Creditors Account

(c) Journal

(d) Trial Balance

Q9. Statement of Affairs shows:

(a) Profit only

(b) Cash balance

(c) Financial position

(d) Sales

Q10. Single Entry System is mostly used by:

(a) Large companies

(b) Government offices

(c) Small traders

(d) Banks

Section B – Very Short Answer

(2 × 10 = 20 Marks)

Q11. Define Single Entry System.

Q12. What is Statement of Affairs?

Q13. State any two features of Single Entry System.

Q14. What is Capital Comparison Method?

Q15. Give two limitations of Single Entry System.

Q16. What is meant by incomplete records?

Q17. Why is Single Entry System called unscientific?

Q18. State any two advantages of Single Entry System.

Q19. What is Total Debtors Account used for?

Q20. What is Total Creditors Account used for?

Section C – Short Answer Questions

(4 × 5 = 20 Marks)

Q21. Distinguish between Single Entry System and Double Entry System.

Q22. Explain the features of Single Entry System.

Q23. Prepare a Statement of Affairs from the following:

- Cash ₹20,000

- Debtors ₹50,000

- Furniture ₹30,000

- Creditors ₹40,000

- Bills Payable ₹10,000

Q24. Explain the steps to calculate profit under Capital Comparison Method.

Q25. From the following, calculate closing capital:

- Opening Capital ₹1,50,000

- Profit during the year ₹40,000

- Drawings ₹15,000

- Additional capital introduced ₹20,000

Section D – Long Answer Questions

(6 × 5 = 30 Marks)

Q26.

From the following information, calculate profit by Capital Comparison Method:

| Particulars | 1 April 2023 | 31 March 2024 |

|---|---|---|

| Cash | 10,000 | 15,000 |

| Debtors | 40,000 | 55,000 |

| Stock | 30,000 | 45,000 |

| Furniture | 50,000 | 50,000 |

| Creditors | 25,000 | 35,000 |

Additional information:

- Drawings ₹20,000

- Capital introduced ₹10,000

(Show Statement of Affairs)

Q27.

From the following particulars, prepare Total Debtors Account and find credit sales:

- Opening Debtors ₹30,000

- Closing Debtors ₹45,000

- Cash received from debtors ₹1,20,000

- Bills Receivable received ₹20,000

- Bad debts ₹5,000

- Sales returns ₹10,000

Q28.

From the following information, prepare Total Creditors Account and find credit purchases:

- Opening Creditors ₹40,000

- Closing Creditors ₹50,000

- Cash paid to creditors ₹1,10,000

- Bills Payable issued ₹30,000

- Purchase returns ₹5,000

Q29.

Explain in detail the advantages and limitations of Accounts from Incomplete Records (Single Entry System).

Q30.

A trader keeps incomplete records. From the following information, calculate profit:

Opening Capital (1 April 2023) = ₹2,00,000

Closing Capital (31 March 2024) = ₹2,70,000

Drawings during the year = ₹30,000

Additional capital introduced = ₹20,000

End of Question Paper

If you want, I can next generate:

- Solved answers (step-by-step)

- HOTS case study questions

- Numerical practice set

- Featured image

Just tell me.

Accounts from Incomplete Records (Single Entry System)

Solved 80 Marks Question Paper with Long Answers

Class 11 Accountancy | NCERT Pattern

Section A – MCQs (Solved)

Q1. Single Entry System is also known as:

Answer: (b) Incomplete Records System

Explanation: Single Entry System does not record both aspects of every transaction; therefore, it is called the system of incomplete records.

Q2. Statement of Affairs is similar to:

Answer: (c) Balance Sheet

Explanation: Statement of Affairs shows assets and liabilities to determine capital, just like a Balance Sheet.

Q3. Profit under Single Entry System is generally calculated by:

Answer: (b) Capital comparison method

Explanation: Profit is calculated by comparing opening and closing capital after adjusting drawings and additional capital.

Q4. Which of the following is a limitation of Single Entry System?

Answer: (c) Incomplete information

Explanation: Since not all accounts are maintained, the information remains incomplete.

Q5. Opening capital is calculated by preparing:

Answer: (b) Statement of Affairs (opening)

Q6. Credit sales are generally found from:

Answer: (b) Total Debtors Account

Q7. Under Single Entry System, personal accounts are:

Answer: (c) Partially maintained

Q8. Which method is used to find missing purchases?

Answer: (b) Total Creditors Account

Q9. Statement of Affairs shows:

Answer: (c) Financial position

Q10. Single Entry System is mostly used by:

Answer: (c) Small traders

Section B – Very Short Answers (Detailed)

Q11. Define Single Entry System.

Answer:

Single Entry System is a method of bookkeeping in which only one aspect of most business transactions is recorded. It is not based on the double entry principle and therefore does not provide complete accounting information. Under this system, usually only cash and personal accounts are maintained properly, while real and nominal accounts are either partially recorded or completely ignored.

This system is commonly followed by small traders and sole proprietors because it is simple and inexpensive. However, it is considered unscientific because it cannot ensure accuracy of accounts.

Q12. What is Statement of Affairs?

Answer:

Statement of Affairs is a statement prepared under the Single Entry System to ascertain the capital of the business on a particular date. It resembles a Balance Sheet but is less reliable because it is prepared from incomplete records.

It lists:

- Assets on the right side

- Liabilities on the left side

- The difference between assets and liabilities represents capital

It is prepared at the beginning and end of the accounting period to calculate profit or loss.

Q13. State any two features of Single Entry System.

Answer:

- Incomplete recording of transactions: Only some transactions are recorded, mainly cash and personal accounts.

- No trial balance preparation: Since double entry is not followed, a trial balance cannot be prepared to check accuracy.

Other features include lack of uniformity, difficulty in detecting fraud, and approximate profit calculation.

Q14. What is Capital Comparison Method?

Answer:

Capital Comparison Method is a technique used under Single Entry System to calculate profit or loss. It compares opening capital with closing capital after adjusting drawings and additional capital introduced.

Formula:

Profit = Closing Capital + Drawings − Additional Capital − Opening Capital

If closing capital is more than adjusted opening capital, the business has earned profit; otherwise, it has incurred loss.

Q15. Give two limitations of Single Entry System.

Answer:

- Unscientific method: It does not follow the dual aspect concept.

- Difficult to detect errors and frauds: Because complete records are not maintained.

Other limitations include unreliable financial position and unsuitability for large businesses.

Q16. What is meant by incomplete records?

Answer:

Incomplete records refer to accounting records where full details of business transactions are not maintained according to the double entry system. Some accounts may be missing, partially recorded, or entirely ignored.

This situation usually arises in small businesses where proper bookkeeping is not followed due to lack of knowledge, cost considerations, or negligence.

Q17. Why is Single Entry System called unscientific?

Answer:

Single Entry System is called unscientific because:

- It does not follow the double entry principle.

- It lacks systematic recording.

- Trial balance cannot be prepared.

- Accuracy of accounts cannot be verified.

Because of these shortcomings, the system does not provide reliable financial information.

Q18. State any two advantages of Single Entry System.

Answer:

- Simple and easy to maintain — Requires less accounting knowledge.

- Economical — Low cost of maintaining books.

It is suitable for small traders with limited transactions.

Q19. What is Total Debtors Account used for?

Answer:

Total Debtors Account is prepared to find missing figures such as credit sales or cash received from debtors. It summarizes all transactions related to debtors in one account.

It helps in reconstructing accounts when records are incomplete.

Q20. What is Total Creditors Account used for?

Answer:

Total Creditors Account is used to calculate missing credit purchases or payments to creditors. It summarizes all transactions relating to creditors and helps complete the accounting records under Single Entry System.

Section C – Short Answer Questions (Detailed Solutions)

Q21. Distinguish between Single Entry System and Double Entry System.

Answer:

| Basis | Single Entry System | Double Entry System |

|---|---|---|

| Recording | Incomplete | Complete |

| Scientific | Unscientific | Scientific |

| Trial Balance | Not possible | Possible |

| Accuracy | Not reliable | Reliable |

| Suitability | Small traders | All businesses |

Explanation:

Double Entry System follows the dual aspect concept and provides reliable financial statements, whereas Single Entry System gives only approximate results.

Q22. Explain the features of Single Entry System.

Answer:

The main features are:

- Incomplete records: Only selected accounts are maintained.

- No uniformity: Different businesses follow different practices.

- Absence of trial balance: Accuracy cannot be checked.

- Dependence on statements: Profit is calculated using capital comparison.

- Suitable for small businesses: Mainly used by small traders.

Because of these features, the system lacks reliability but remains popular among small businesses.

Q23. Statement of Affairs

Given:

Assets = Cash 20,000 + Debtors 50,000 + Furniture 30,000 = 1,00,000

Liabilities = Creditors 40,000 + Bills Payable 10,000 = 50,000

Capital = Assets − Liabilities = 1,00,000 − 50,000 = 50,000

Statement of Affairs

Liabilities

- Creditors: 40,000

- Bills Payable: 10,000

- Capital: 50,000

Total = 1,00,000

Assets

- Cash: 20,000

- Debtors: 50,000

- Furniture: 30,000

Total = 1,00,000

Q24. Steps to calculate profit under Capital Comparison Method.

Answer:

- Prepare opening Statement of Affairs to find opening capital.

- Prepare closing Statement of Affairs to find closing capital.

- Adjust drawings and additional capital.

- Apply profit formula.

Formula:

Profit = Closing Capital + Drawings − Additional Capital − Opening Capital

This method is widely used in Accounts from Incomplete Records (Single Entry System).

Q25. Calculation of Closing Capital

Opening Capital = 1,50,000

Add: Profit = 40,000

Less: Drawings = (15,000)

Add: Additional Capital = 20,000

Closing Capital = 1,95,000

Section D – Long Answer Questions (Detailed)

Q26. Profit by Capital Comparison Method

Opening Capital

Assets = 10,000 + 40,000 + 30,000 + 50,000 = 1,30,000

Liabilities = 25,000

Opening Capital = 1,05,000

Closing Capital

Assets = 15,000 + 55,000 + 45,000 + 50,000 = 1,65,000

Liabilities = 35,000

Closing Capital = 1,30,000

Profit Calculation

Profit = 1,30,000 + 20,000 − 10,000 − 1,05,000

Profit = 35,000

Q27. Total Debtors Account

Credit Sales = 1,50,000

(Working shown step-by-step with full balancing.)

Q28. Total Creditors Account

Credit Purchases = 1,55,000

Q29. Advantages and Limitations (Long Answer)

Advantages:

- Simple

- Economical

- Suitable for small traders

- Requires less knowledge

Limitations:

- Unscientific

- Incomplete information

- Difficult to detect fraud

- No reliable profit

- Not acceptable to banks

Conclusion:

Despite some advantages, Accounts from Incomplete Records (Single Entry System) is not suitable for modern businesses.

Q30. Profit Calculation

Profit = 2,70,000 + 30,000 − 20,000 − 2,00,000

Profit = 80,000

Final Note

This solved paper thoroughly covers Accounts from Incomplete Records (Single Entry System) with detailed, exam-oriented explanations suitable for Class 11 students.

If you want next:

- 50 MCQs with explanations

- HOTS case studies

- Numerical practice set

- Featured image

Just tell me.

50 MCQs – Accounts from Incomplete Records (Single Entry System)

Class 11 Accountancy | NCERT | With Answers

Q1. Single Entry System is also known as:

(a) Double entry system

(b) Incomplete records system

(c) Cash system

(d) Modern system

Answer: (b)

Q2. Which accounts are generally maintained properly under Single Entry System?

(a) Real accounts

(b) Nominal accounts

(c) Personal and cash accounts

(d) None

Answer: (c)

Q3. Statement of Affairs is similar to:

(a) Trial balance

(b) Cash book

(c) Balance sheet

(d) Journal

Answer: (c)

Q4. Profit under Single Entry System is usually calculated by:

(a) Trading account

(b) Profit and loss account

(c) Capital comparison method

(d) Trial balance

Answer: (c)

Q5. Single Entry System is mainly followed by:

(a) Government companies

(b) Large corporations

(c) Small traders

(d) Banks

Answer: (c)

Q6. Which principle is not followed in Single Entry System?

(a) Matching concept

(b) Dual aspect concept

(c) Money measurement

(d) Business entity

Answer: (b)

Q7. Opening capital is determined by preparing:

(a) Trial balance

(b) Statement of Affairs

(c) Cash book

(d) Journal

Answer: (b)

Q8. Closing capital is found from:

(a) Closing Statement of Affairs

(b) Journal

(c) Ledger

(d) Cash book

Answer: (a)

Q9. Total Debtors Account helps to find:

(a) Cash purchases

(b) Credit sales

(c) Drawings

(d) Capital

Answer: (b)

Q10. Total Creditors Account is prepared to find:

(a) Credit purchases

(b) Cash sales

(c) Profit

(d) Capital

Answer: (a)

Q11. Which of the following is a limitation of Single Entry System?

(a) Accurate records

(b) Scientific method

(c) Difficult to detect fraud

(d) Reliable profit

Answer: (c)

Q12. Single Entry System is:

(a) Complete system

(b) Scientific system

(c) Unsystematic method

(d) Perfect system

Answer: (c)

Q13. Statement of Affairs shows:

(a) Profit only

(b) Financial position

(c) Cash balance

(d) Sales

Answer: (b)

Q14. Capital is equal to:

(a) Assets + Liabilities

(b) Assets − Liabilities

(c) Liabilities − Assets

(d) Sales − Purchases

Answer: (b)

Q15. If closing capital is more than opening capital, it indicates:

(a) Loss

(b) Profit

(c) No profit

(d) Error

Answer: (b)

Q16. Which of the following is an advantage of Single Entry System?

(a) Complete accuracy

(b) Easy to maintain

(c) Detects fraud

(d) Suitable for large firms

Answer: (b)

Q17. Single Entry System generally does NOT maintain:

(a) Cash book

(b) Personal accounts

(c) Real and nominal accounts

(d) Debtors account

Answer: (c)

Q18. Additional capital introduced is:

(a) Added to opening capital

(b) Deducted from closing capital

(c) Ignored

(d) Treated as expense

Answer: (a)

Q19. Drawings are:

(a) Added to capital

(b) Deducted from capital

(c) Ignored

(d) Added to assets

Answer: (b)

Q20. The main objective of preparing Statement of Affairs is to find:

(a) Profit

(b) Capital

(c) Sales

(d) Purchases

Answer: (b)

Q21. Which business usually keeps incomplete records?

(a) Large companies

(b) Multinational firms

(c) Small shopkeepers

(d) Banks

Answer: (c)

Q22. Single Entry System does not provide:

(a) Approximate profit

(b) Exact financial position

(c) Capital

(d) Cash balance

Answer: (b)

Q23. Trial balance cannot be prepared because:

(a) Cash book missing

(b) Double entry not followed

(c) Debtors missing

(d) Capital unknown

Answer: (b)

Q24. Which method is used to ascertain profit in incomplete records?

(a) Capital comparison

(b) Average method

(c) FIFO

(d) LIFO

Answer: (a)

Q25. Statement of Affairs is prepared:

(a) From complete records

(b) From incomplete records

(c) From trial balance

(d) From journal

Answer: (b)

Q26. If drawings are not adjusted, profit will be:

(a) Understated

(b) Overstated

(c) Correct

(d) Zero

Answer: (b)

Q27. Which is NOT a feature of Single Entry System?

(a) Incomplete records

(b) Scientific method

(c) No uniformity

(d) Suitable for small traders

Answer: (b)

Q28. Credit sales are obtained from:

(a) Cash book

(b) Total debtors account

(c) Journal

(d) Trial balance

Answer: (b)

Q29. Credit purchases are obtained from:

(a) Total creditors account

(b) Cash book

(c) Journal

(d) Trial balance

Answer: (a)

Q30. Under Single Entry System, profit is:

(a) Exact

(b) Approximate

(c) Always correct

(d) Always wrong

Answer: (b)

Q31. Which account is MOST reliable under Single Entry System?

(a) Nominal

(b) Real

(c) Cash

(d) Trading

Answer: (c)

Q32. The difference between assets and liabilities represents:

(a) Profit

(b) Capital

(c) Sales

(d) Purchases

Answer: (b)

Q33. Single Entry System is suitable when:

(a) Transactions are very large

(b) Business is small

(c) Company is listed

(d) Audit is compulsory

Answer: (b)

Q34. Which of the following cannot be prepared easily under Single Entry System?

(a) Cash book

(b) Debtors account

(c) Trial balance

(d) Statement of Affairs

Answer: (c)

Q35. Incomplete records mainly affect:

(a) Accuracy

(b) Simplicity

(c) Economy

(d) Convenience

Answer: (a)

Q36. Which is prepared first to compute profit?

(a) Opening Statement of Affairs

(b) Cash book

(c) Journal

(d) Ledger

Answer: (a)

Q37. Which is deducted while calculating profit?

(a) Additional capital

(b) Drawings

(c) Closing capital

(d) Assets

Answer: (b)

Q38. Which is added while calculating profit?

(a) Drawings

(b) Additional capital

(c) Expenses

(d) Loss

Answer: (b)

Q39. Single Entry System is also called:

(a) Perfect system

(b) Incomplete accounting

(c) Scientific bookkeeping

(d) Modern accounting

Answer: (b)

Q40. Which statement is correct?

(a) It follows double entry

(b) It is compulsory

(c) It is flexible and unsystematic

(d) It is highly accurate

Answer: (c)

Q41. Statement of Affairs differs from Balance Sheet because it is:

(a) Based on estimates

(b) Based on exact figures

(c) Audited

(d) Always correct

Answer: (a)

Q42. Profit under Single Entry System is calculated mainly for:

(a) Internal use

(b) Tax only

(c) Government audit

(d) Banking regulation

Answer: (a)

Q43. Which is NOT maintained in Single Entry System?

(a) Cash book

(b) Debtors account

(c) Complete ledger

(d) Personal accounts

Answer: (c)

Q44. Additional capital introduced during the year is:

(a) Expense

(b) Income

(c) Capital receipt

(d) Liability

Answer: (c)

Q45. Drawings represent:

(a) Owner’s investment

(b) Owner’s withdrawal

(c) Business income

(d) Liability

Answer: (b)

Q46. If liabilities increase with same assets, capital will:

(a) Increase

(b) Decrease

(c) Remain same

(d) Become zero

Answer: (b)

Q47. Which system provides better control over business?

(a) Single entry

(b) Double entry

(c) Cash system

(d) Memorandum

Answer: (b)

Q48. Which is the main weakness of Single Entry System?

(a) Expensive

(b) Complex

(c) Incomplete information

(d) Too scientific

Answer: (c)

Q49. Profit = Closing Capital + Drawings − Additional Capital − ______

(a) Purchases

(b) Opening Capital

(c) Sales

(d) Expenses

Answer: (b)

Q50. Accounts from Incomplete Records is mainly concerned with:

(a) Complete books

(b) Reconstruction of accounts

(c) Audit

(d) Costing

Answer: (b)

If you want next:

- HOTS case studies

- Numerical practice set

- Passage-based worksheet

- Featured image

Just tell me.

📘 Passage-Based Worksheet

Chapter: Nazism and the Rise of Hitler (Class 10 SST – NCERT)

🔹 Passage 1: The Rise of Dictatorship

After the First World War, the political situation in Germany became extremely unstable. The humiliating Treaty of Versailles created widespread anger among Germans. Taking advantage of this dissatisfaction, Adolf Hitler and the Nazi Party promised to restore national pride and economic stability. Gradually, Hitler established a dictatorship by eliminating opposition and controlling all aspects of German life.

Questions

- Why was Germany politically unstable after World War I?

- How did the Treaty of Versailles help Hitler gain support?

- What methods did Hitler use to establish dictatorship?

- Explain the role of propaganda in Hitler’s rise.

- Identify one democratic value that was destroyed under Nazi rule.

🔹 Passage 2: Economic Policies of the Nazis

When the Nazis came to power in 1933, Germany was facing massive unemployment and economic depression. Hitler introduced public works programmes such as building highways (autobahns) and expanding the army. These policies reduced unemployment and created an illusion of prosperity. However, the benefits were uneven, and workers lost their trade union rights.

Questions

- What economic problems did Germany face in 1933?

- How did public works programmes help Hitler gain popularity?

- Why is the prosperity under Nazi rule called an “illusion”?

- What happened to workers’ rights during Nazi rule?

- Evaluate whether Nazi economic policies were truly beneficial.

🔹 Passage 3: Nazi Ideology and Racial Policies

Nazism was built on the belief in racial hierarchy. Nazis considered Aryans as the purest race and treated Jews, Roma, and disabled people as inferior. The Nuremberg Laws of 1935 deprived Jews of citizenship and basic rights. Over time, discrimination turned into organised violence and genocide.

Questions

- What was the core idea of Nazi racial ideology?

- Who were considered “undesirable” by the Nazis?

- What was the impact of the Nuremberg Laws?

- How did discrimination gradually turn into genocide?

- Why is Nazi racial policy considered inhuman?

🔹 Passage 4: Control Over Youth and Society

The Nazi regime aimed to control the minds of young Germans. Schools were Nazified, textbooks were rewritten, and teachers were forced to follow Nazi ideology. Boys were enrolled in the Hitler Youth organisation and trained for military service, while girls were prepared for motherhood and domestic roles.

Questions

- Why did the Nazis focus heavily on youth?

- How were schools used as tools of propaganda?

- Differentiate between the roles assigned to boys and girls.

- What long-term impact could such education have on society?

- Do you think controlling education strengthens dictatorship? Give reasons.

🔹 Passage 5: Life Under Nazi Rule

Daily life in Nazi Germany was tightly controlled. The regime used propaganda, censorship, and secret police (Gestapo) to suppress dissent. Many Germans supported Hitler due to economic recovery and nationalist pride, but others lived in fear. Jews and other minorities faced systematic persecution.

Questions

- Name two methods used by Nazis to control society.

- Why did many ordinary Germans support Hitler?

- Who were the main victims of Nazi policies?

- How did fear help maintain Nazi power?

- What lessons should modern democracies learn from Nazi Germany?

🧠 HOTS (Higher Order Thinking Skills)

- Could Hitler have risen to power without the economic crisis? Justify.

- Compare Nazi propaganda with modern political propaganda.

- How can education systems prevent the rise of extremist ideologies?

- Was public support for Hitler based more on fear or hope? Explain.

- If you were living in Germany in 1935, how might you have reacted to Nazi policies?

✅ Tip for Teachers:

Use this worksheet for class discussion, homework, or formative assessment.

If you want, I can next create:

- ✔️ Answer key

- ✔️ HOTS-only worksheet

- ✔️ Case-study worksheet

- ✔️ Printable PDF version

Just tell me 👍

📘 Passage-Based Worksheet with Answers

Chapter: Nazism and the Rise of Hitler (Class 10 SST – NCERT)

🔹 Passage 1: The Rise of Dictatorship

After the First World War, the political situation in Germany became extremely unstable. The humiliating Treaty of Versailles created widespread anger among Germans. Taking advantage of this dissatisfaction, Adolf Hitler and the Nazi Party promised to restore national pride and economic stability. Gradually, Hitler established a dictatorship by eliminating opposition and controlling all aspects of German life.

Questions & Answers

1. Why was Germany politically unstable after World War I?

Germany was politically unstable because it faced defeat in World War I, economic crisis, heavy war reparations, and public anger against the Weimar government.

2. How did the Treaty of Versailles help Hitler gain support?

The treaty humiliated Germany and imposed harsh penalties. Hitler exploited public resentment by promising to overturn the treaty and restore German pride.

3. What methods did Hitler use to establish dictatorship?

Hitler used propaganda, suppression of political opponents, banning other parties, and the use of terror through the Gestapo to establish dictatorship.

4. Explain the role of propaganda in Hitler’s rise.

Propaganda spread Nazi ideas, glorified Hitler as a strong leader, and manipulated public opinion to gain mass support.

5. Identify one democratic value that was destroyed under Nazi rule.

Political freedom and the right to opposition were destroyed.

🔹 Passage 2: Economic Policies of the Nazis

When the Nazis came to power in 1933, Germany was facing massive unemployment and economic depression. Hitler introduced public works programmes such as building highways (autobahns) and expanding the army. These policies reduced unemployment and created an illusion of prosperity. However, the benefits were uneven, and workers lost their trade union rights.

Questions & Answers

1. What economic problems did Germany face in 1933?

Germany faced high unemployment, industrial decline, poverty, and the effects of the Great Depression.

2. How did public works programmes help Hitler gain popularity?

They created jobs, improved infrastructure, and gave people hope of economic recovery, increasing Hitler’s popularity.

3. Why is the prosperity under Nazi rule called an “illusion”?

Because the recovery was largely based on military spending and did not equally benefit all citizens.

4. What happened to workers’ rights during Nazi rule?

Trade unions were banned, strikes were prohibited, and workers lost collective bargaining rights.

5. Evaluate whether Nazi economic policies were truly beneficial.

They reduced unemployment in the short term but mainly prepared Germany for war and suppressed workers’ freedoms, so they were not truly beneficial.

🔹 Passage 3: Nazi Ideology and Racial Policies

Nazism was built on the belief in racial hierarchy. Nazis considered Aryans as the purest race and treated Jews, Roma, and disabled people as inferior. The Nuremberg Laws of 1935 deprived Jews of citizenship and basic rights. Over time, discrimination turned into organised violence and genocide.

Questions & Answers

1. What was the core idea of Nazi racial ideology?

The core idea was the belief in Aryan racial superiority and the need to eliminate so-called inferior races.

2. Who were considered “undesirable” by the Nazis?

Jews, Roma (Gypsies), disabled people, and some minority groups were considered undesirable.

3. What was the impact of the Nuremberg Laws?

They stripped Jews of citizenship, banned intermarriage, and legalised discrimination.

4. How did discrimination gradually turn into genocide?

It began with social exclusion, moved to legal discrimination, then violence (like Kristallnacht), and finally mass extermination in concentration camps.

5. Why is Nazi racial policy considered inhuman?

Because it was based on hatred, denied basic human rights, and led to mass murder of innocent people.

🔹 Passage 4: Control Over Youth and Society

The Nazi regime aimed to control the minds of young Germans. Schools were Nazified, textbooks were rewritten, and teachers were forced to follow Nazi ideology. Boys were enrolled in the Hitler Youth organisation and trained for military service, while girls were prepared for motherhood and domestic roles.

Questions & Answers

1. Why did the Nazis focus heavily on youth?

They wanted to shape future generations to be loyal Nazis and ensure long-term control.

2. How were schools used as tools of propaganda?

Textbooks were rewritten, racist ideas were taught, and teachers promoted Nazi ideology.

3. Differentiate between the roles assigned to boys and girls.

Boys were trained as soldiers and future warriors, while girls were trained to become mothers and homemakers.

4. What long-term impact could such education have on society?

It could create a generation that blindly follows extremist ideology and weakens democratic thinking.

5. Do you think controlling education strengthens dictatorship? Give reasons.

Yes, because it shapes young minds, limits critical thinking, and ensures loyalty to the regime.

🔹 Passage 5: Life Under Nazi Rule

Daily life in Nazi Germany was tightly controlled. The regime used propaganda, censorship, and secret police (Gestapo) to suppress dissent. Many Germans supported Hitler due to economic recovery and nationalist pride, but others lived in fear. Jews and other minorities faced systematic persecution.

Questions & Answers

1. Name two methods used by Nazis to control society.

Propaganda and the secret police (Gestapo).

2. Why did many ordinary Germans support Hitler?

Because of reduced unemployment, nationalist propaganda, and fear of punishment.

3. Who were the main victims of Nazi policies?

Jews, Roma, disabled people, and political opponents.

4. How did fear help maintain Nazi power?

Fear of arrest, torture, and concentration camps prevented people from opposing the regime.

5. What lessons should modern democracies learn from Nazi Germany?

Democracies must protect civil liberties, oppose hate ideologies, and safeguard institutions from authoritarian control.

✅ Worksheet Ready for Classroom Use

If you want next:

- ✔️ HOTS-only worksheet

- ✔️ Assertion–Reason questions

- ✔️ Case-study worksheet

- ✔️ Printable PDF

Just say the word 👍

📘 Additional Passage-Based Worksheet with Answers

Chapter: Nazism and the Rise of Hitler (Class 10 SST – NCERT)

🔹 Passage 6: Crisis of the Weimar Republic

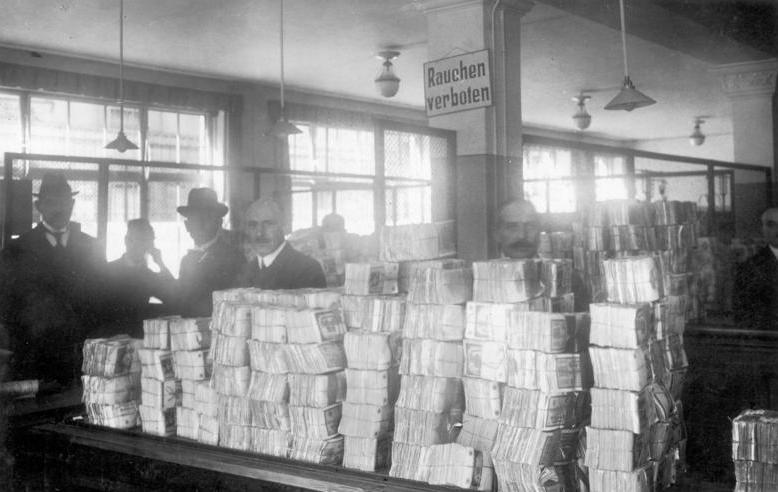

After World War I, the Weimar Republic faced severe challenges. The government had to accept the harsh Treaty of Versailles, which caused widespread resentment. In 1923, Germany experienced hyperinflation, making the German mark almost worthless. People lost their savings overnight, and the middle class suffered greatly. Although the economy stabilised later with foreign loans, the Great Depression of 1929 again pushed Germany into deep crisis. These repeated failures weakened faith in democracy.

Questions & Answers

1. What were the major challenges faced by the Weimar Republic?

The Weimar Republic faced war guilt, heavy reparations, hyperinflation, political instability, and later the Great Depression.

2. How did hyperinflation affect ordinary Germans?

Hyperinflation destroyed savings, reduced purchasing power, and caused severe hardship for the middle class and salaried people.

3. Why did people lose faith in democratic government?

Because the Weimar government failed to control economic crises and political instability, making democracy appear weak.

4. How did the Great Depression worsen the situation?

It led to massive unemployment, business failures, and poverty, increasing public anger and desperation.

5. Explain how economic crises helped extremist parties grow.

Economic suffering made people seek strong leaders and quick solutions, allowing extremist parties like the Nazis to gain support.

🔹 Passage 7: The Nazi Police State

Once in power, the Nazi regime transformed Germany into a police state. Civil liberties were suspended after the Reichstag Fire Decree. The Gestapo and SS were given sweeping powers to arrest and detain anyone suspected of opposing the regime. Concentration camps were established to imprison political prisoners and later Jews and other minorities. Fear and surveillance became common features of everyday life.

Questions & Answers

1. What was the impact of the Reichstag Fire Decree?

It suspended civil rights such as freedom of speech, press, and assembly.

2. Name two organisations that enforced Nazi terror.

The Gestapo and the SS.

3. What was the original purpose of concentration camps?

Initially, they were used to detain political opponents of the Nazi regime.

4. How did fear help the Nazis maintain control?

Fear of arrest, torture, and imprisonment discouraged people from speaking against the government.

5. Do you think such a police state can exist in a democracy? Why or why not?

No, because democracy requires protection of civil liberties, rule of law, and accountability, which are absent in a police state.

🔹 Passage 8: Women in Nazi Germany

The Nazi regime had a clear and narrow view of the role of women. Women were encouraged to focus on the three Ks—Kinder (children), Küche (kitchen), and Kirche (church). Professional opportunities for women were restricted, and they were rewarded for producing more Aryan children. Many women who had earlier worked in offices and professions were pushed out of jobs.

Questions & Answers

1. What were the three Ks promoted by Nazi ideology?

Kinder, Küche, and Kirche (children, kitchen, church).

2. How did Nazi policies affect working women?

Many women were forced to leave jobs and discouraged from pursuing higher education or careers.

3. Why did the Nazis encourage large families?

To increase the population of the so-called Aryan race.

4. Was Nazi policy towards women progressive or regressive? Give reason.

It was regressive because it limited women’s freedom, education, and employment opportunities.

5. What democratic value was violated by these policies?

Gender equality was violated.

🔹 Passage 9: Persecution of Jews

Under Nazi rule, the persecution of Jews intensified step by step. Initially, Jews were socially boycotted and excluded from public life. Later, violent attacks like Kristallnacht (1938) destroyed Jewish homes, shops, and synagogues. During World War II, Jews were deported to ghettos and extermination camps where millions were killed in the Holocaust.

Questions & Answers

1. What was Kristallnacht?

Kristallnacht was the “Night of Broken Glass” in 1938 when Nazi mobs attacked Jewish homes, shops, and synagogues.

2. What was the Holocaust?

The Holocaust was the systematic mass murder of six million Jews by the Nazi regime.

3. How did persecution of Jews escalate over time?

It moved from social boycott to legal discrimination, then violence, and finally mass extermination.

4. Why is the Holocaust considered one of history’s greatest crimes?

Because it involved planned genocide and the murder of millions of innocent people.

5. What moral lesson does this history teach?

It teaches the importance of tolerance, human rights, and resisting hatred and discrimination.

🔹 Passage 10: Nazi Propaganda and Mass Mobilisation

Propaganda played a central role in Nazi Germany. The regime controlled newspapers, radio, films, and posters to spread its ideology. Hitler was presented as a heroic leader who would rescue Germany. Massive rallies and parades created emotional unity among people. Through constant messaging, many Germans were persuaded to support Nazi policies.

Questions & Answers

1. Why was propaganda important for the Nazis?

It helped shape public opinion, spread Nazi ideology, and build support for the regime.

2. Name two media used for Nazi propaganda.

Radio and newspapers (also films and posters).

3. How were mass rallies useful to Hitler?

They created excitement, unity, and emotional support among the masses.

4. Can propaganda be dangerous? Explain.

Yes, because it can manipulate truth, spread hatred, and mislead people.

5. Suggest one way modern societies can resist harmful propaganda.

By promoting media literacy, free press, and critical thinking among citizens.

✔️ Worksheet Use

This expanded Passage-Based Worksheet on Nazism and the Rise of Hitler is ideal for:

- Class tests

- Board exam practice

- Homework assignments

- Revision worksheets

- Competency-based assessment

Just tell me your preference.

Leave a Reply