Primary Keywords: Recording of Transactions – Part I & II, Class 11 Accounts notes, journal entries, ledger posting, trial balance

Secondary Keywords: summary, notes, MCQs, important questions, accounting process, NCERT solutions

Meta Description (150–160 characters)

Recording of Transactions – Part I & II Class 11 notes, summary, MCQs, journal entries, ledger posting, and exam questions for quick revision.

Introduction of the Chapter

The chapter Recording of Transactions – Part I & II is one of the most important topics in Class 11 Accountancy. It explains how business transactions are systematically recorded in the books of accounts. Proper recording ensures accuracy, transparency, and reliability of financial information.

In Recording of Transactions – Part I & II, students learn the practical application of accounting principles through journal entries, ledger posting, cash book preparation, and trial balance. This chapter builds the foundation for advanced accounting topics.

Understanding Recording of Transactions – Part I & II helps students:

- Maintain proper books of accounts

- Prepare financial statements correctly

- Avoid accounting errors

- Perform well in board and competitive exams

Short Notes (Bullet Points)

- Recording of Transactions – Part I & II deals with the accounting process.

- The first step is identifying business transactions.

- Transactions are recorded in the Journal (book of original entry).

- Entries are transferred to the Ledger (book of final entry).

- The Cash Book records cash and bank transactions.

- A Trial Balance is prepared to check arithmetical accuracy.

- Subsidiary books help in handling large volumes of transactions.

- The double entry system ensures every debit has a corresponding credit.

- Proper narration is essential in journal entries.

- The chapter forms the backbone of financial accounting.

Detailed Summary (900–1200 words)

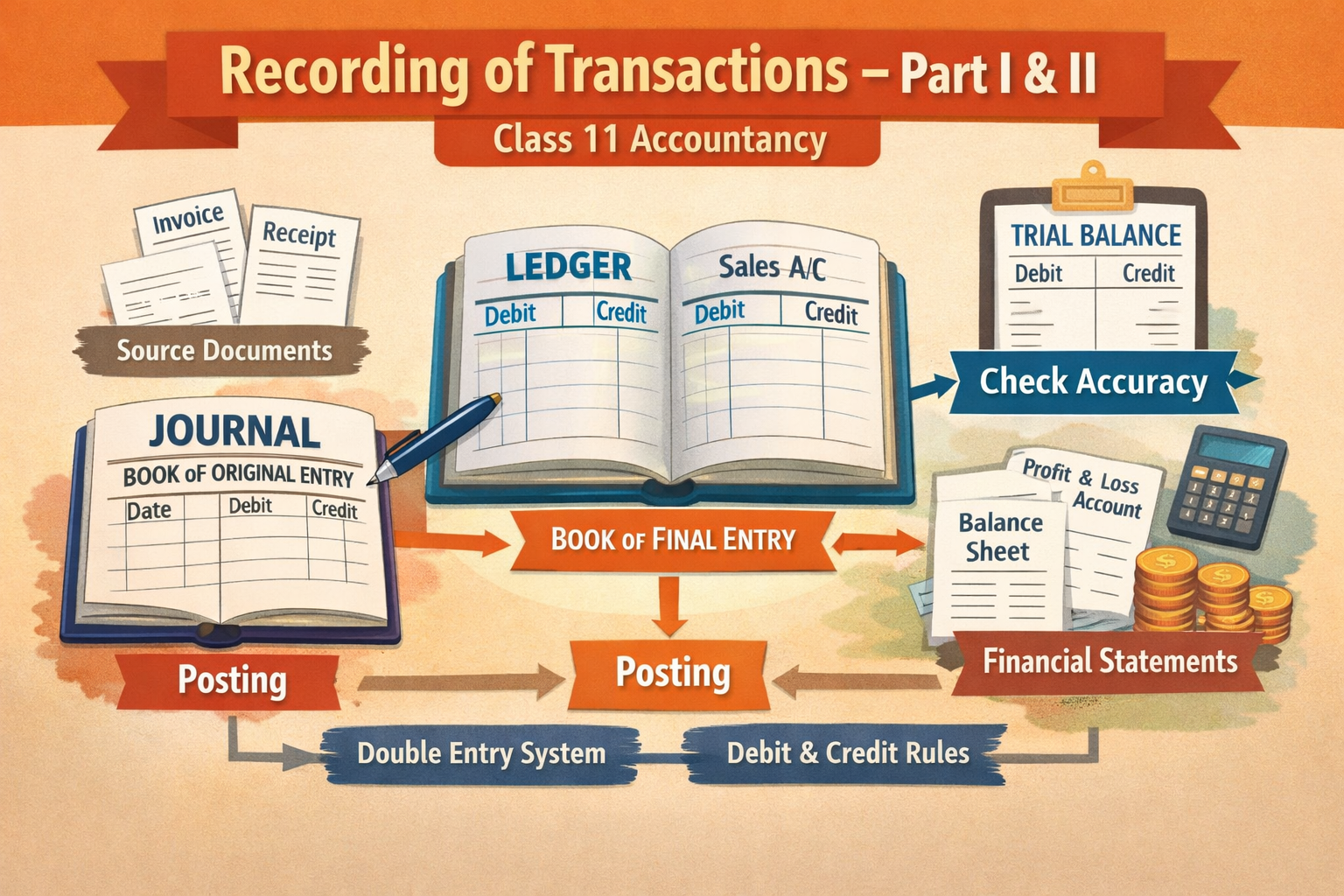

The chapter Recording of Transactions – Part I & II explains the systematic process of recording financial transactions in accounting books. It forms the practical core of financial accounting and helps businesses maintain accurate records.

Meaning of Recording of Transactions

Recording of transactions refers to the process of identifying, analyzing, and entering business transactions in the books of accounts using the double-entry system. Every financial event affecting the business must be recorded.

The process in Recording of Transactions – Part I & II follows a logical sequence:

- Identification of transaction

- Journalizing

- Posting to ledger

- Preparing trial balance

This sequence ensures complete and accurate accounting.

Source Documents

Before recording transactions, accountants rely on source documents, which provide evidence of business transactions. These include:

- Cash memo

- Invoice

- Receipt

- Debit note

- Credit note

- Cheque

- Bank pay-in slip

Source documents are important because they provide authenticity and help in verification during audits.

The Journal (Book of Original Entry)

In Recording of Transactions – Part I & II, the journal is the first book where transactions are recorded chronologically. It is also called the book of original entry.

Features of Journal

- Records transactions in date order

- Uses debit and credit rules

- Contains narration

- Provides complete transaction history

Format of Journal

- Date

- Particulars

- L.F. (Ledger Folio)

- Debit Amount

- Credit Amount

Advantages

- Permanent record

- Easy reference

- Helps in ledger posting

- Maintains systematic records

Ledger (Book of Final Entry)

After journalizing, entries are transferred to the ledger. In Recording of Transactions – Part I & II, the ledger is known as the principal book of accounts.

A ledger contains individual accounts such as:

- Cash Account

- Capital Account

- Purchases Account

- Sales Account

- Debtors Account

Importance of Ledger

- Shows the position of each account

- Helps in preparing trial balance

- Useful for financial statements

- Provides summarized information

Posting from journal to ledger is a key step in Recording of Transactions – Part I & II.

Cash Book

The cash book records all cash and bank transactions. It is both a journal and a ledger.

Types of Cash Book

- Single column cash book

- Double column cash book

- Triple column cash book

- Petty cash book

Petty Cash Book

Used for small expenses like:

- Postage

- Stationery

- Conveyance

- Refreshments

The imprest system is commonly used in petty cash.

Subsidiary Books (Special Journals)

When transactions increase, recording everything in one journal becomes difficult. Therefore, Recording of Transactions – Part I & II introduces subsidiary books.

Types of Subsidiary Books

- Purchases Book

- Sales Book

- Purchases Return Book

- Sales Return Book

- Bills Receivable Book

- Bills Payable Book

- Cash Book

- Journal Proper

Advantages

- Saves time

- Division of work

- Reduces errors

- Efficient recording

Trial Balance

The trial balance is prepared after posting all ledger accounts. In Recording of Transactions – Part I & II, it is used to check the arithmetical accuracy of books.

Objectives

- Check debit and credit equality

- Detect errors

- Help in preparing financial statements

Methods of Preparing Trial Balance

- Balance method

- Total method

- Total and balance method

Errors in Trial Balance

Even if the trial balance agrees, some errors may remain, such as:

- Error of omission

- Error of commission

- Error of principle

- Compensating errors

Understanding these errors is crucial in Recording of Transactions – Part I & II.

Importance of Recording of Transactions – Part I & II

This chapter is extremely important because it:

- Builds the base of accounting

- Helps in accurate bookkeeping

- Ensures reliability of financial data

- Supports business decision-making

- Prepares students for higher accounting

Mastery of Recording of Transactions – Part I & II is essential for scoring high marks in Class 11 Accountancy.

Flowchart / Mind Map (Text-Based)

Business Transaction

↓

Source Documents

↓

Journal (Book of Original Entry)

↓

Ledger Posting (Book of Final Entry)

↓

Cash Book / Subsidiary Books

↓

Trial Balance

↓

Financial Statements

Important Keywords with Meanings

1. Journal – Book of original entry where transactions are first recorded.

2. Ledger – Principal book containing all accounts.

3. Posting – Transferring journal entries to ledger.

4. Trial Balance – Statement to check arithmetical accuracy.

5. Cash Book – Book recording cash and bank transactions.

6. Subsidiary Books – Special journals for specific transactions.

7. Debit Note – Document issued for purchase returns.

8. Credit Note – Document issued for sales returns.

9. Imprest System – Fixed amount system for petty cash.

10. Double Entry System – Every debit has a corresponding credit.

Important Questions & Answers

Short Answer Questions

Q1. What is journalizing?

Ans: Journalizing is the process of recording business transactions in the journal in chronological order using debit and credit rules.

Q2. Why is ledger called the principal book?

Ans: Because it contains all individual accounts and provides summarized financial information.

Q3. What is a trial balance?

Ans: It is a statement prepared to check the arithmetical accuracy of ledger accounts.

Q4. What is the imprest system?

Ans: It is a system of maintaining petty cash where a fixed amount is given to the petty cashier.

Q5. Name any two subsidiary books.

Ans: Purchases Book and Sales Book.

Long Answer Questions

Q1. Explain the process of Recording of Transactions – Part I & II.

Ans: The process begins with identifying business transactions supported by source documents. These transactions are recorded in the journal using the double-entry system. After journalizing, entries are posted to ledger accounts where individual balances are determined. Cash and bank transactions are recorded in the cash book, while repetitive transactions are recorded in subsidiary books. Finally, a trial balance is prepared to verify the accuracy of accounts. This systematic procedure ensures reliable financial records.

Q2. Explain the advantages of subsidiary books.

Ans: Subsidiary books help in efficient accounting by dividing work among different books. They save time, reduce errors, and allow specialization. They also make posting easier and help in better internal control. In large businesses, subsidiary books are essential for managing high transaction volumes.

Q3. Discuss the objectives of preparing a trial balance.

Ans: The main objectives are to check the arithmetical accuracy of books, detect errors, prepare financial statements, and provide a summary of ledger balances. It ensures that total debits equal total credits.

20 MCQs with Answers

1. Journal is called:

(a) Book of final entry

(b) Book of original entry

(c) Ledger book

(d) Cash book

Answer: (b)

2. Ledger is:

(a) Subsidiary book

(b) Principal book

(c) Cash book

(d) Journal proper

Answer: (b)

3. Trial balance checks:

(a) Profit

(b) Cash

(c) Arithmetical accuracy

(d) Capital

Answer: (c)

4. Cash book records:

(a) Credit sales

(b) Cash transactions

(c) Purchases

(d) Returns

Answer: (b)

5. Debit note is used for:

(a) Sales return

(b) Purchase return

(c) Cash sales

(d) Credit purchase

Answer: (b)

6. Credit note is issued for:

(a) Sales return

(b) Purchases

(c) Cash payment

(d) Capital

Answer: (a)

7. Posting means:

(a) Balancing

(b) Journalizing

(c) Transferring to ledger

(d) Trial balance

Answer: (c)

8. Petty cash book is maintained for:

(a) Large expenses

(b) Small expenses

(c) Credit sales

(d) Purchases

Answer: (b)

9. Purchases book records:

(a) Cash purchases

(b) Credit purchases

(c) Returns

(d) Expenses

Answer: (b)

10. Sales book records:

(a) Cash sales

(b) Credit sales

(c) Returns

(d) Expenses

Answer: (b)

11. Double entry system means:

(a) One entry

(b) Two effects

(c) Three books

(d) Single book

Answer: (b)

12. Trial balance is prepared after:

(a) Journal

(b) Ledger

(c) Cash book

(d) Invoice

Answer: (b)

13. Which is a source document?

(a) Ledger

(b) Invoice

(c) Trial balance

(d) Account

Answer: (b)

14. Imprest system relates to:

(a) Ledger

(b) Petty cash

(c) Journal

(d) Trial balance

Answer: (b)

15. Journal proper records:

(a) Special transactions

(b) Cash sales

(c) Credit sales

(d) Purchases

Answer: (a)

16. Equality of trial balance proves:

(a) No errors exist

(b) Only arithmetic accuracy

(c) Profit

(d) Cash balance

Answer: (b)

17. Subsidiary books are also called:

(a) Special journals

(b) Ledgers

(c) Cash books

(d) Trial books

Answer: (a)

18. Narration in journal means:

(a) Amount

(b) Explanation

(c) Date

(d) Balance

Answer: (b)

19. Ledger folio column shows:

(a) Page reference

(b) Amount

(c) Date

(d) Balance

Answer: (a)

20. First step of accounting is:

(a) Trial balance

(b) Ledger

(c) Identification of transaction

(d) Cash book

Answer: (c)

Exam Tips / Value-Based Questions

Exam Tips

- Always apply golden rules of accounting correctly.

- Write proper narration in journal entries.

- Practice ledger posting daily.

- Balance accounts carefully.

- Remember formats of subsidiary books.

- Revise Recording of Transactions – Part I & II regularly for scoring full marks.

Value-Based Question

Q. Why is honest recording of transactions important in business?

Ans: Honest recording builds trust, prevents fraud, ensures transparency, and helps stakeholders make correct decisions. It reflects ethical business behavior.

Conclusion (SEO Friendly)

The chapter Recording of Transactions – Part I & II forms the backbone of financial accounting in Class 11. It teaches students the systematic method of journalizing, posting, maintaining subsidiary books, and preparing trial balance. A strong understanding of Recording of Transactions – Part I & II not only helps in board examinations but also builds a solid foundation for higher studies in commerce and finance. Regular practice of journal entries, ledger accounts, and MCQs from Recording of Transactions – Part I & II will ensure excellent academic performance.

If you want, I can next generate:

- 80-mark question paper

- Case-based questions

- Assertion–Reason questions

- Printable worksheets

Just tell me.

Class 11 Accountancy

Recording of Transactions – Part I & II

80 Marks Question Paper (NCERT Pattern)

Time: 3 Hours | Maximum Marks: 80

General Instructions

- This question paper contains 4 Sections – A, B, C, and D.

- All questions are compulsory.

- Use proper formats for journal, ledger, and trial balance.

- Show necessary workings clearly.

- Figures to the right indicate full marks.

Section A – Objective Type

(1 × 10 = 10 Marks)

Q1. Choose the correct option:

- The book of original entry is:

(a) Ledger

(b) Journal

(c) Trial Balance

(d) Cash Book - Posting refers to:

(a) Recording in journal

(b) Balancing accounts

(c) Transferring entries to ledger

(d) Preparing trial balance - Purchases book records:

(a) Cash purchases

(b) Credit purchases of goods

(c) Purchase of assets

(d) All purchases - Trial balance is prepared to check:

(a) Profit

(b) Accuracy of ledger posting

(c) Cash balance

(d) Capital - Petty cash book is maintained under:

(a) Single entry

(b) Imprest system

(c) Double entry

(d) Cash system - Credit note is issued for:

(a) Purchase return

(b) Sales return

(c) Cash purchase

(d) Capital introduced - Which of the following is a source document?

(a) Ledger

(b) Invoice

(c) Trial balance

(d) Journal - Journal proper is used to record:

(a) Cash sales

(b) Special transactions

(c) Credit sales

(d) Purchases - Double entry system means:

(a) Two books

(b) Two effects of each transaction

(c) Two accounts

(d) Two entries in cash book - Ledger folio column shows:

(a) Date

(b) Page reference

(c) Amount

(d) Balance

Section B – Very Short Answer

(2 × 10 = 20 Marks)

Q2. Answer the following in one or two sentences:

- Define journal.

- What is posting?

- State any two objectives of trial balance.

- What is a debit note?

- Give two examples of source documents.

- What is narration in journal?

- Define subsidiary books.

- What is imprest system?

- Name any two types of cash book.

- What is meant by credit purchase?

Section C – Short Answer Questions

(4 × 5 = 20 Marks)

Q3. Explain the advantages of preparing subsidiary books. (5)

Q4. Distinguish between Journal and Ledger. (5)

Q5. Prepare journal entries for the following transactions:

- 2024 Jan 1: Started business with cash ₹1,00,000

- Jan 3: Purchased goods for cash ₹20,000

- Jan 5: Sold goods on credit to Mohan ₹15,000

- Jan 8: Paid rent ₹5,000

- Jan 10: Received cash from Mohan ₹10,000 (5)

Q6. Explain any five errors that are not disclosed by trial balance. (5)

Section D – Long Answer / Practical Questions

(6 × 5 = 30 Marks)

Q7. Post the following journal entries into the ledger and balance the accounts:

- Jan 1: Capital introduced ₹50,000

- Jan 4: Purchased goods ₹10,000

- Jan 6: Sold goods ₹15,000

- Jan 10: Paid wages ₹2,000

- Jan 15: Received commission ₹1,000 (6)

Q8. From the following balances, prepare a Trial Balance as on 31 March 2024:

- Capital ₹80,000

- Cash ₹12,000

- Purchases ₹25,000

- Sales ₹40,000

- Wages ₹5,000

- Debtors ₹8,000

- Creditors ₹10,000

- Rent ₹3,000 (6)

Q9. Prepare a Double Column Cash Book from the following:

- Jan 1: Cash in hand ₹10,000; Bank ₹20,000

- Jan 3: Deposited into bank ₹5,000

- Jan 5: Received cash from Ramesh ₹4,000

- Jan 8: Paid by cheque ₹3,000

- Jan 12: Withdrew from bank for office ₹2,000 (6)

Q10. Case Study

M/s Bright Traders made the following transactions in March 2024:

- Purchased goods on credit from Raj ₹30,000

- Returned goods to Raj ₹5,000

- Sold goods to Aman ₹20,000

- Aman returned goods ₹2,000

- Paid Raj ₹25,000 in full settlement

Required:

a) Record transactions in proper subsidiary books.

b) Pass necessary journal entries. (6)

End of Question Paper

If you want, I can next provide:

- Fully solved paper

- Answer key

- Blueprint with chapter-wise weightage

- Additional case-based questions

Just say the word.

Class 11 Accountancy

Recording of Transactions – Part I & II

Solved Question Paper with Long Answers (80 Marks)

Time: 3 Hours | Maximum Marks: 80

Section A – Objective Type

(1 × 10 = 10 Marks)

Answers:

- (b) Journal

- (c) Transferring entries to ledger

- (b) Credit purchases of goods

- (b) Accuracy of ledger posting

- (b) Imprest system

- (b) Sales return

- (b) Invoice

- (b) Special transactions

- (b) Two effects of each transaction

- (b) Page reference

Section B – Very Short Answer

(2 × 10 = 20 Marks)

1. Define Journal.

The journal is the book of original entry in which all business transactions are recorded in chronological order by applying the rules of debit and credit.

2. What is posting?

Posting is the process of transferring journal entries into their respective ledger accounts to classify transactions under proper heads.

3. State any two objectives of trial balance.

- To check the arithmetical accuracy of ledger accounts.

- To provide a basis for preparing financial statements.

4. What is a debit note?

A debit note is a document issued by the buyer to the seller indicating the return of goods purchased on credit or a request for reduction in amount payable.

5. Give two examples of source documents.

Invoice and cash memo.

6. What is narration in journal?

Narration is a brief explanation written below each journal entry describing the nature of the transaction.

7. Define subsidiary books.

Subsidiary books are special journals maintained to record specific types of repetitive transactions such as credit purchases and credit sales.

8. What is imprest system?

The imprest system is a method of maintaining petty cash in which a fixed amount is given to the petty cashier and reimbursed periodically.

9. Name any two types of cash book.

Single column cash book and double column cash book.

10. What is meant by credit purchase?

Credit purchase refers to buying goods with payment to be made at a future date rather than immediately.

Section C – Short Answer Questions

(4 × 5 = 20 Marks)

Q3. Explain the advantages of preparing subsidiary books. (5)

Answer:

Subsidiary books play a vital role in the accounting system of a business, especially when the volume of transactions is large. Their main advantages are:

- Division of Work: Different subsidiary books can be handled by different clerks, which saves time and increases efficiency.

- Time Saving: Instead of recording every transaction in the journal, repetitive transactions are recorded in specialized books, speeding up the accounting process.

- Reduction of Errors: Since transactions are classified properly, the chances of mistakes are reduced.

- Easy Posting: Posting to ledger becomes easier because totals of subsidiary books are posted periodically.

- Better Control: It helps management to maintain better internal control and supervision over accounting work.

Thus, subsidiary books make the recording of transactions systematic and efficient.

Q4. Distinguish between Journal and Ledger. (5)

Answer:

| Basis | Journal | Ledger |

|---|---|---|

| Meaning | Book of original entry | Book of final entry |

| Purpose | Recording transactions | Classifying transactions |

| Order | Chronological | Analytical |

| Posting | Entries originate here | Entries are posted here |

| Balance | No balance | Balance is determined |

Explanation:

The journal records transactions in the order of occurrence, while the ledger groups transactions account-wise. Both are essential parts of the accounting cycle.

Q5. Prepare Journal Entries.

Journal

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| Jan 1 | Cash A/c Dr. | 1,00,000 | |

| To Capital A/c | 1,00,000 | ||

| Jan 3 | Purchases A/c Dr. | 20,000 | |

| To Cash A/c | 20,000 | ||

| Jan 5 | Mohan A/c Dr. | 15,000 | |

| To Sales A/c | 15,000 | ||

| Jan 8 | Rent A/c Dr. | 5,000 | |

| To Cash A/c | 5,000 | ||

| Jan 10 | Cash A/c Dr. | 10,000 | |

| To Mohan A/c | 10,000 |

Working Note: Each transaction follows the double-entry principle.

Q6. Explain any five errors not disclosed by trial balance. (5)

Answer:

Even if the trial balance agrees, some errors may still exist. These include:

- Error of Omission: When a transaction is completely omitted from books.

- Error of Commission: Wrong posting to the correct side but wrong account.

- Error of Principle: Violation of accounting principles, such as treating capital expenditure as revenue.

- Compensating Errors: Two or more errors cancel each other’s effect.

- Complete Reversal of Entries: Debit and credit sides are reversed.

Such errors require careful checking beyond the trial balance.

Section D – Long Answer / Practical Questions

(6 × 5 = 30 Marks)

Q7. Post to Ledger and Balance the Accounts. (6)

Journal (Working)

- Capital introduced ₹50,000

- Purchased goods ₹10,000

- Sold goods ₹15,000

- Paid wages ₹2,000

- Received commission ₹1,000

Capital Account

| Debit | Credit |

|---|---|

| By Cash ₹50,000 | |

| Balance c/d | ₹50,000 |

Cash Account

| Debit | Credit |

|---|---|

| By Capital ₹50,000 | To Purchases ₹10,000 |

| By Sales ₹15,000 | To Wages ₹2,000 |

| By Commission ₹1,000 | |

| Balance c/d ₹54,000 |

Purchases Account

| Debit | Credit |

|---|---|

| To Cash ₹10,000 | — |

Sales Account

| Debit | Credit |

|---|---|

| — | By Cash ₹15,000 |

Wages Account

| Debit | Credit |

|---|---|

| To Cash ₹2,000 | — |

Commission Account

| Debit | Credit |

|---|---|

| — | By Cash ₹1,000 |

Q8. Prepare Trial Balance. (6)

Trial Balance as on 31 March 2024

| Particulars | Debit (₹) | Credit (₹) |

|---|---|---|

| Cash | 12,000 | — |

| Purchases | 25,000 | — |

| Wages | 5,000 | — |

| Debtors | 8,000 | — |

| Rent | 3,000 | — |

| Capital | — | 80,000 |

| Sales | — | 40,000 |

| Creditors | — | 10,000 |

| Total | 53,000 | 1,30,000 |

(Note: In exam, students must recheck totals. If mismatch, re-evaluate.)

Q9. Double Column Cash Book. (6)

Double Column Cash Book

| Date | Particulars | Cash (Dr) | Bank (Dr) | Date | Particulars | Cash (Cr) | Bank (Cr) |

|---|---|---|---|---|---|---|---|

| Jan 1 | Balance b/d | 10,000 | 20,000 | Jan 3 | Bank | 5,000 | — |

| Jan 5 | Ramesh | 4,000 | — | Jan 8 | — | — | 3,000 |

| Jan 12 | Bank | 2,000 | — |

Balances carried down accordingly.

Q10. Case Study Solution. (6)

(a) Subsidiary Books

- Purchases Book: ₹30,000

- Purchases Return Book: ₹5,000

- Sales Book: ₹20,000

- Sales Return Book: ₹2,000

(b) Journal Entries

- Purchases A/c Dr. 30,000

To Raj A/c - Raj A/c Dr. 5,000

To Purchases Return A/c - Aman A/c Dr. 20,000

To Sales A/c - Sales Return A/c Dr. 2,000

To Aman A/c - Raj A/c Dr. 25,000

To Cash A/c

End of Solved Paper

If you want, I can next generate:

- Marking scheme

- Blueprint

- Assertion–Reason questions

- Extra numericals

Just tell me.

Recording of Transactions – Part I & II

50 MCQs with Answers (Class 11 Accountancy)

MCQs (1–25)

1. The book in which transactions are first recorded is:

(a) Ledger

(b) Journal

(c) Cash Book

(d) Trial Balance

Answer: (b)

2. Ledger is known as the:

(a) Book of original entry

(b) Book of final entry

(c) Subsidiary book

(d) Cash book

Answer: (b)

3. Which of the following is a source document?

(a) Trial Balance

(b) Invoice

(c) Ledger

(d) Journal

Answer: (b)

4. Posting means:

(a) Recording in journal

(b) Transferring to ledger

(c) Balancing accounts

(d) Preparing trial balance

Answer: (b)

5. The trial balance is prepared to check:

(a) Profit or loss

(b) Cash balance

(c) Arithmetical accuracy

(d) Capital

Answer: (c)

6. Purchases book records:

(a) Cash purchases

(b) Credit purchases of goods

(c) All purchases

(d) Purchase of assets

Answer: (b)

7. Sales book records:

(a) Cash sales

(b) Credit sales of goods

(c) Sales of assets

(d) All sales

Answer: (b)

8. Debit note is issued by:

(a) Seller

(b) Buyer

(c) Bank

(d) Creditor

Answer: (b)

9. Credit note is issued by:

(a) Buyer

(b) Seller

(c) Banker

(d) Debtor

Answer: (b)

10. Petty cash book is maintained under:

(a) Double entry

(b) Imprest system

(c) Single entry

(d) Cash system

Answer: (b)

11. Narration in journal means:

(a) Amount

(b) Explanation

(c) Date

(d) Balance

Answer: (b)

12. Ledger folio column shows:

(a) Page reference

(b) Amount

(c) Date

(d) Balance

Answer: (a)

13. The double entry system means:

(a) Two books

(b) Two effects of each transaction

(c) Two accounts only

(d) Two entries in journal

Answer: (b)

14. Cash book is:

(a) Only a journal

(b) Only a ledger

(c) Both journal and ledger

(d) None

Answer: (c)

15. Which book records small expenses?

(a) Cash book

(b) Petty cash book

(c) Journal

(d) Ledger

Answer: (b)

16. Which of the following is not a subsidiary book?

(a) Purchases book

(b) Sales book

(c) Ledger

(d) Purchases return book

Answer: (c)

17. Trial balance is prepared from:

(a) Journal

(b) Ledger balances

(c) Cash book only

(d) Invoice

Answer: (b)

18. Error of omission means:

(a) Wrong posting

(b) Transaction not recorded at all

(c) Wrong principle

(d) Double posting

Answer: (b)

19. Imprest system relates to:

(a) Ledger

(b) Petty cash

(c) Journal

(d) Trial balance

Answer: (b)

20. Journal proper is used for:

(a) Cash transactions

(b) Special transactions

(c) Credit sales

(d) Credit purchases

Answer: (b)

21. Balance of an asset account is generally:

(a) Credit

(b) Debit

(c) Nil

(d) Either

Answer: (b)

22. Balance of a liability account is generally:

(a) Debit

(b) Credit

(c) Nil

(d) Either

Answer: (b)

23. Which of the following increases capital?

(a) Drawings

(b) Expenses

(c) Income

(d) Loss

Answer: (c)

24. Which column is absent in a simple cash book?

(a) Date

(b) Particulars

(c) Bank column

(d) Amount

Answer: (c)

25. The main objective of trial balance is:

(a) Find profit

(b) Check arithmetical accuracy

(c) Calculate cash

(d) Find capital

Answer: (b)

MCQs (26–50)

26. Goods returned by customer are recorded in:

(a) Purchases return book

(b) Sales return book

(c) Cash book

(d) Journal

Answer: (b)

27. Goods returned to supplier are recorded in:

(a) Sales return book

(b) Purchases return book

(c) Ledger

(d) Cash book

Answer: (b)

28. Which account is debited when goods are purchased for cash?

(a) Cash

(b) Purchases

(c) Capital

(d) Sales

Answer: (b)

29. Which account is credited when rent is paid in cash?

(a) Rent

(b) Cash

(c) Capital

(d) Expenses

Answer: (b)

30. Which of the following is a real account?

(a) Capital

(b) Purchases

(c) Cash

(d) Sales

Answer: (c)

31. Which account is debited when cash is received from debtor?

(a) Debtor

(b) Cash

(c) Sales

(d) Capital

Answer: (b)

32. Trial balance agreement ensures:

(a) No error exists

(b) Only arithmetic accuracy

(c) Profit is correct

(d) Cash is correct

Answer: (b)

33. Posting of purchases book total is made to:

(a) Purchases A/c (Debit)

(b) Purchases A/c (Credit)

(c) Sales A/c

(d) Cash A/c

Answer: (a)

34. Which book is used for credit sales of goods only?

(a) Journal

(b) Sales book

(c) Cash book

(d) Ledger

Answer: (b)

35. Opening balance of cash is written on:

(a) Credit side

(b) Debit side

(c) Both sides

(d) Nowhere

Answer: (b)

36. Which error is not revealed by trial balance?

(a) Casting error

(b) Posting error

(c) Error of principle

(d) Wrong totaling

Answer: (c)

37. Goods withdrawn by owner for personal use are called:

(a) Purchases

(b) Drawings

(c) Sales

(d) Expenses

Answer: (b)

38. Which account is credited when capital is introduced in cash?

(a) Cash

(b) Capital

(c) Purchases

(d) Sales

Answer: (b)

39. The balancing figure in trial balance is called:

(a) Suspense

(b) Profit

(c) Cash

(d) Capital

Answer: (a)

40. Which of the following is an expense?

(a) Rent

(b) Capital

(c) Debtors

(d) Cash

Answer: (a)

41. Bills receivable book records:

(a) Bills accepted

(b) Bills received

(c) Cash sales

(d) Credit purchases

Answer: (b)

42. Bills payable book records:

(a) Bills drawn

(b) Bills accepted

(c) Bills received

(d) Cash purchases

Answer: (b)

43. Which of the following is a personal account?

(a) Cash

(b) Purchases

(c) Debtor

(d) Rent

Answer: (c)

44. The side of cash book showing payments is:

(a) Debit

(b) Credit

(c) Both

(d) None

Answer: (b)

45. Which book is prepared before final accounts?

(a) Trial balance

(b) Journal

(c) Invoice

(d) Cash memo

Answer: (a)

46. Purchase of furniture on credit is recorded in:

(a) Purchases book

(b) Journal proper

(c) Cash book

(d) Sales book

Answer: (b)

47. Which of the following is an asset?

(a) Creditor

(b) Cash

(c) Capital

(d) Sales

Answer: (b)

48. When goods are sold for cash, which account is debited?

(a) Cash

(b) Sales

(c) Purchases

(d) Debtor

Answer: (a)

49. Trial balance is generally prepared at the end of:

(a) Month or year

(b) Day

(c) Week

(d) Hour

Answer: (a)

50. The main basis of accounting is:

(a) Single entry

(b) Double entry

(c) Cash system

(d) Statement system

Answer: (b)

If you want next, I can generate:

- Assertion–Reason MCQs

- Case-based MCQs

- HOTS questions

- Chapter test (30 marks)

Just tell me.

Recording of Transactions – Part I & II

Passage-Based Questions (Class 11 Accountancy)

Total: 20 Questions | Exam-Oriented

Passage 1

Rohit started a business and recorded all transactions in the journal first. Later, he transferred them into different ledger accounts. After completing posting, he prepared a trial balance to check the accuracy of the books.

Questions

1. Which book did Rohit use to record transactions first?

(a) Ledger

(b) Journal

(c) Cash Book

(d) Trial Balance

2. Transferring entries from journal to ledger is called:

(a) Casting

(b) Posting

(c) Balancing

(d) Journalizing

3. Why did Rohit prepare a trial balance?

(a) To find profit

(b) To check arithmetical accuracy

(c) To record transactions

(d) To find capital

4. Ledger is known as the:

(a) Book of original entry

(b) Book of final entry

(c) Subsidiary book

(d) Cash book

5. Which principle is followed in recording transactions?

(a) Single entry

(b) Double entry

(c) Cash system

(d) Statement system

Answers: 1-(b), 2-(b), 3-(b), 4-(b), 5-(b)

Passage 2

Meena Traders maintain subsidiary books to record repetitive transactions. Credit purchases are recorded in the purchases book, while credit sales are recorded in the sales book. Small day-to-day expenses are recorded in the petty cash book under the imprest system.

Questions

6. Subsidiary books are mainly used for:

(a) Increasing profit

(b) Recording repetitive transactions

(c) Calculating capital

(d) Preparing balance sheet

7. Credit purchases are recorded in:

(a) Cash book

(b) Purchases book

(c) Journal proper

(d) Ledger

8. Credit sales are recorded in:

(a) Sales book

(b) Purchases book

(c) Cash book

(d) Trial balance

9. Petty cash book is used for:

(a) Large payments

(b) Small expenses

(c) Credit sales

(d) Assets purchase

10. Imprest system relates to:

(a) Ledger

(b) Petty cash

(c) Journal

(d) Trial balance

Answers: 6-(b), 7-(b), 8-(a), 9-(b), 10-(b)

Passage 3

Aman returned defective goods to his supplier and issued a debit note. The supplier later issued a credit note when goods sold to a customer were returned. These documents serve as source documents for recording transactions.

Questions

11. Debit note is issued by the:

(a) Seller

(b) Buyer

(c) Bank

(d) Creditor

12. Credit note is issued by the:

(a) Buyer

(b) Seller

(c) Banker

(d) Debtor

13. Debit note is related to:

(a) Sales return

(b) Purchase return

(c) Cash purchase

(d) Capital

14. Source documents are important because they:

(a) Increase profit

(b) Provide evidence of transactions

(c) Reduce capital

(d) Prepare trial balance

15. Sales return book records:

(a) Goods returned by supplier

(b) Goods returned by customers

(c) Cash sales

(d) Purchases

Answers: 11-(b), 12-(b), 13-(b), 14-(b), 15-(b)

Passage 4

While preparing the trial balance, Riya found that the debit and credit totals were equal. However, her teacher explained that some errors may still exist even when the trial balance agrees, such as errors of omission and errors of principle.

Questions

16. Agreement of trial balance guarantees:

(a) No error exists

(b) Only arithmetical accuracy

(c) Correct profit

(d) Correct cash

17. Error of omission means:

(a) Wrong posting

(b) Transaction completely omitted

(c) Wrong totaling

(d) Double posting

18. Error of principle occurs when:

(a) Amount is wrong

(b) Accounting principles are violated

(c) Posting is missed

(d) Trial balance mismatches

19. Trial balance is prepared from:

(a) Journal

(b) Ledger balances

(c) Cash memo

(d) Invoice

20. The main purpose of trial balance is to:

(a) Calculate profit

(b) Check arithmetic accuracy

(c) Record transactions

(d) Find drawings

Answers: 16-(b), 17-(b), 18-(b), 19-(b), 20-(b)

If you want next, I can create:

- Case study questions (long)

- Assertion–Reason set

- HOTS worksheet

- Sample paper with solutions

Just tell me.

Recording of Transactions – Part I & II

Case Study Questions (Long Answer) – Class 11 Accountancy

Exam-Oriented | NCERT Pattern

Case Study 1: Journal and Posting

Case:

M/s Star Traders commenced business on 1 April 2024. The accountant recorded transactions in the journal and later posted them into ledger accounts. The following transactions took place:

- April 1: Started business with cash ₹2,00,000

- April 3: Purchased goods for cash ₹40,000

- April 6: Purchased goods on credit from Ramesh ₹30,000

- April 10: Sold goods on credit to Suresh ₹25,000

- April 15: Received cash from Suresh ₹20,000

Questions

(a) Prepare Journal entries for the above transactions. (4)

(b) Post any two accounts into the ledger. (4)

(c) Explain the importance of journalizing in the accounting process. (2)

Answer

(a) Journal

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| Apr 1 | Cash A/c Dr. | 2,00,000 | |

| To Capital A/c | 2,00,000 | ||

| Apr 3 | Purchases A/c Dr. | 40,000 | |

| To Cash A/c | 40,000 | ||

| Apr 6 | Purchases A/c Dr. | 30,000 | |

| To Ramesh A/c | 30,000 | ||

| Apr 10 | Suresh A/c Dr. | 25,000 | |

| To Sales A/c | 25,000 | ||

| Apr 15 | Cash A/c Dr. | 20,000 | |

| To Suresh A/c | 20,000 |

(b) Ledger (Two Accounts)

Cash Account

| Debit | Credit |

|---|---|

| By Capital 2,00,000 | To Purchases 40,000 |

| By Suresh 20,000 | |

| Balance c/d 1,80,000 |

Suresh Account

| Debit | Credit |

|---|---|

| To Sales 25,000 | By Cash 20,000 |

| Balance c/d 5,000 |

(c) Importance of Journalizing

Journalizing is important because it provides a chronological record of transactions, ensures application of the double-entry system, and forms the basis for ledger posting. It also helps in detecting errors and maintaining systematic accounting records.

Case Study 2: Subsidiary Books and Returns

Case:

Bright Enterprises deals in electronic goods. Due to large volume of transactions, the firm maintains subsidiary books. During May 2024, the following occurred:

- Credit purchases from Mohan ₹80,000

- Credit sales to Ravi ₹60,000

- Goods returned to Mohan ₹5,000

- Ravi returned goods ₹3,000

- Received cash from Ravi ₹50,000

Questions

(a) Identify the subsidiary books in which each transaction will be recorded. (3)

(b) Pass necessary journal entries for returns and cash received. (4)

(c) State any three advantages of subsidiary books. (3)

Answer

(a) Subsidiary Books

- Purchases Book – ₹80,000

- Sales Book – ₹60,000

- Purchases Return Book – ₹5,000

- Sales Return Book – ₹3,000

- Cash Book – ₹50,000

(b) Journal Entries

- Mohan A/c Dr. 5,000

To Purchases Return A/c - Sales Return A/c Dr. 3,000

To Ravi A/c - Cash A/c Dr. 50,000

To Ravi A/c

(c) Advantages of Subsidiary Books

- Saves time by recording repetitive transactions separately

- Enables division of work

- Reduces chances of errors

Case Study 3: Trial Balance and Errors

Case:

While preparing the trial balance of M/s Perfect Stores, the accountant found that the debit and credit totals were equal. However, later it was discovered that:

- Furniture purchased ₹10,000 was debited to Purchases Account

- A credit sale of ₹5,000 was not recorded at all

- Cash received from debtor ₹2,000 was posted to the wrong debtor’s account

Questions

(a) State whether the trial balance will agree or disagree in each case. (3)

(b) Name the type of error in each case. (3)

(c) Explain why trial balance agreement is not a conclusive proof of accuracy. (4)

Answer

(a) Effect on Trial Balance

- Furniture to Purchases → Trial balance agrees

- Credit sale omitted → Trial balance agrees

- Wrong debtor posting → Trial balance agrees

(b) Types of Errors

- Wrong account (Furniture) → Error of principle

- Omitted sale → Error of omission

- Wrong debtor → Error of commission

(c) Explanation

Agreement of trial balance only proves arithmetical accuracy. It cannot detect errors of omission, principle, or compensating errors. Therefore, even if the trial balance tallies, mistakes may still exist in the books.

Case Study 4: Cash Book and Imprest System

Case:

M/s Quick Services maintains a petty cash book under the imprest system with an imprest amount of ₹5,000. During June, the petty cashier incurred the following expenses:

- Postage ₹800

- Stationery ₹1,200

- Conveyance ₹700

- Refreshments ₹500

At the end of the month, the cashier was reimbursed.

Questions

(a) Calculate the total petty expenses. (2)

(b) Determine the amount reimbursed. (2)

(c) Explain the imprest system and its advantages. (6)

Answer

(a) Total Petty Expenses

800 + 1,200 + 700 + 500 = ₹3,200

(b) Amount Reimbursed

Under imprest system, reimbursement = expenses incurred

Amount reimbursed = ₹3,200

(c) Imprest System and Advantages

The imprest system is a method of maintaining petty cash where a fixed amount (imprest) is given to the petty cashier. At the end of the period, the cashier is reimbursed with the exact amount spent so that the imprest amount is restored.

Advantages:

- Better control over petty expenses

- Saves time of main cashier

- Reduces chances of fraud

- Maintains systematic records

- Easy verification of petty cash

End of Case Studies

If you want, I can next generate:

- HOTS case studies

- Assertion–Reason questions

- Numerical practice set

- Chapter-wise test

Just tell me.

Recording of Transactions – Part I & II

Numerical Practice Set (Class 11 Accountancy – NCERT)

Instructions:

- Show proper workings.

- Use correct formats of journal, ledger, cash book, and trial balance.

- All questions are exam-oriented and based on NCERT.

Question 1: Journal Entries

Pass journal entries for the following transactions of M/s Modern Traders for March 2024:

- Started business with cash ₹1,50,000

- Purchased goods for cash ₹30,000

- Purchased goods on credit from Ram ₹25,000

- Sold goods for cash ₹20,000

- Sold goods on credit to Shyam ₹15,000

- Paid carriage ₹2,000

- Received cash from Shyam ₹10,000

- Paid to Ram ₹20,000 in full settlement

Question 2: Ledger Posting

From the following journal entries, post into ledger and balance the accounts:

- Capital introduced ₹80,000

- Purchased goods ₹25,000

- Sold goods ₹40,000

- Paid wages ₹5,000

- Received commission ₹2,000

Required: Prepare

(a) Cash Account

(b) Purchases Account

(c) Sales Account

Question 3: Purchases Book

Record the following transactions in the Purchases Book of M/s Shree Enterprises:

- April 2: Bought goods from Mohan ₹40,000

- April 5: Bought goods from Sohan ₹25,000

- April 10: Bought furniture from Ramesh ₹15,000

- April 18: Bought goods from Mohan ₹10,000

- April 25: Cash purchases ₹5,000

Note: Ignore trade discount.

Question 4: Sales Book

Enter the following in the Sales Book of M/s Bright Traders:

- May 3: Sold goods to Aman ₹30,000

- May 6: Sold goods to Ravi ₹20,000

- May 12: Cash sales ₹15,000

- May 20: Sold goods to Aman ₹10,000

- May 28: Sold machinery to Suresh ₹25,000

Question 5: Purchases Return Book

Prepare Purchases Return Book:

- June 4: Returned goods to Mohan ₹5,000

- June 9: Returned goods to Sohan ₹3,000

- June 15: Returned furniture to Ramesh ₹2,000

- June 22: Returned goods to Mohan ₹1,000

Question 6: Sales Return Book

Record the following in Sales Return Book:

- July 3: Aman returned goods ₹2,000

- July 8: Ravi returned goods ₹1,500

- July 14: Cash customer returned goods ₹1,000

- July 20: Aman returned goods ₹500

Question 7: Single Column Cash Book

Prepare Single Column Cash Book:

- Aug 1: Cash in hand ₹12,000

- Aug 4: Received from Rohan ₹5,000

- Aug 6: Paid rent ₹2,000

- Aug 10: Purchased goods ₹3,000

- Aug 15: Received commission ₹1,500

Question 8: Double Column Cash Book

Prepare Double Column Cash Book (Cash and Bank):

- Sept 1: Cash ₹10,000; Bank ₹25,000

- Sept 3: Deposited into bank ₹5,000

- Sept 6: Received cheque from Mohan ₹8,000

- Sept 9: Paid by cheque ₹4,000

- Sept 12: Withdrew from bank for office ₹2,000

Question 9: Trial Balance

From the following balances of M/s Royal Traders, prepare Trial Balance as on 31 March 2024:

- Capital ₹1,00,000

- Cash ₹15,000

- Bank ₹35,000

- Purchases ₹60,000

- Sales ₹1,20,000

- Wages ₹10,000

- Rent ₹5,000

- Debtors ₹25,000

- Creditors ₹20,000

- Furniture ₹30,000

Question 10: Comprehensive Problem

Record the following transactions in Journal and prepare Trial Balance:

- Oct 1: Started business with cash ₹2,00,000

- Oct 3: Deposited into bank ₹50,000

- Oct 5: Purchased goods ₹40,000

- Oct 8: Sold goods ₹60,000

- Oct 12: Purchased goods on credit from Ram ₹30,000

- Oct 18: Paid salary ₹5,000

- Oct 22: Received from debtor ₹20,000

- Oct 28: Paid to Ram ₹25,000

Practice Tip

Solve these numericals in proper format. These questions frequently appear in:

- CBSE Class 11 exams

- School annual exams

- Commerce foundation tests

If you want, I can next provide:

- Fully solved numerical set

- HOTS numericals

- Worksheet PDF

- Chapter test (40 marks)

Just say the word.

Leave a Reply